Should I Ask For 10K Off The Purchase Price Or Closing Costs? Fargo–Moorhead & West Fargo Guide

Imagine this:

You find a house you love.

You're ready to write an offer.

But then your lender and I start talking strategy, and you hear a sentence that sounds a little scary:

"We could ask for ten thousand off the price, or ten thousand in seller-paid closing costs."

Both options sound like $10,000 dollars to you, and if you're like most people, you nod your head, pretend you understand, and then go home and think,

"I really hope I don't make a $10,000 dollar mistake."

These kinds of questions and worries shouldn't keep you up at night. So, below, I'll walk you through this choice in simple terms, the way I explain it to buyers in the Fargo, Moorhead, and West Fargo area.

Before I get started, it's important to note that all the numbers in this article are examples only, not rate quotes or promises. Interest rates, closing costs, and loan guidelines change often, so it's best to have us run your exact numbers before we structure an offer.

The $10,000 Question No One Explains

Let us keep this simple.

There are two main ways that the same $10,000 can show up in your offer:

- $10,000 dollars off the price

- $10,000 dollars the seller pays toward your closing costs

On paper, those look almost identical. In real life, they behave very differently. Here's the basic idea:

- Taking $10K off the price mostly helps you over time

- Getting $10K in seller-paid costs mostly helps you on day one

One speaks to your future self.

The other speaks to your right now self.

You need to know which version of you is louder at this stage of life.

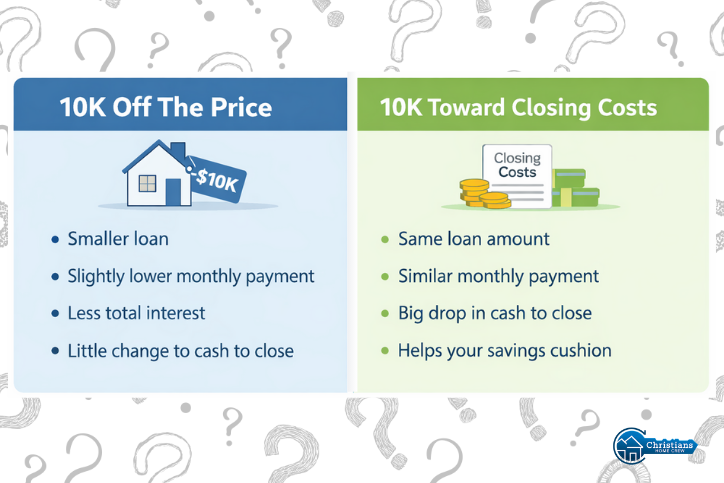

Option 1: Asking for $10,000 Off the Price

Imagine you are buying a home for around $325,000, which is a typical amount in our area for a financed buyer.

If you negotiate the purchase price down to $315,000, it usually means

- Your loan amount is smaller

- Your monthly payment is a little lower

- Over the life of the loan, you pay less total interest

Here's an example using a buyer's typical 30-year fixed loan:

- Getting $10,000 off the purchase price lowered their payment by about $60 per month

- It also cut their total interest bill by roughly $12,000 over thirty years

Your numbers will differ, of course, but this gives you some sense of the scale.

The catch with this option is simple.

You still have to bring your own closing costs and prepaids to the table. The price is lower, but the cash you need up front does not necessarily change very much.

This option is best for you if you:

- plan to stay put for a while

- have the cash for closing and still keep a cushion in savings

- care a lot about paying less interest over the long run

If that sounds like you, $10,000 off the price can be a strong long-term move.

Option 2: Asking for $10,000 Toward Your Closing Costs

Now let us look at the other path.

Same house, same $325,000. Instead of dropping the price, you ask the seller to keep the price as is and instead pay $10,000 toward your closing costs.

Side note: this is usually called "Seller paid closing costs," "Seller credits," or "Seller concessions."

In this case, typically:

- Your loan amount stays higher, because the price did not change

- Your monthly payment stays about the same if your interest rate stays the same

- The seller's $10,000 goes toward things like:

- Lender fees

- Title and closing fees

- Prepaid taxes and insurance, depending on how your loan is structured

In the kind of example we often see in West Fargo, Fargo, and Moorhead, that $10,000 might knock down the amount of cash you'll need to close by several thousand dollars, sometimes close to the full $10,000 amount, depending on your exact costs and program limits.

Instead of bringing something like $25,000 to closing, you might bring something closer to around $15,000 in that kind of example. The exact figures will depend on your loan, down payment, taxes, insurance, and other details your lender will calculate.

That upfront closing cost can make a huge difference for a lot of families.

This option is best for you if you:

- are tight on cash after down payment, inspection, and moving costs

- want to keep some money in savings for emergencies, kids, or early repairs

- feel okay about the monthly payment, but are nervous about emptying your bank account

If that sounds like you, $10K in seller-paid costs can feel like a big relief.

A Simple Way To Picture The Difference

In a typical Fargo–Moorhead style scenario, when we compare these two choices side by side, the pattern often looks something like this:

Same 10,000 dollars. Two very different kinds of help.

One helps your monthly budget and your long-term interest.

The other helps your savings account and your stress level on closing day.

Neither is automatically "better." The better option is the one that solves the bigger problem for you right now.

We can show you your own version of this comparison so you are not guessing.

What About Using 10K To Lower Your Interest Rate?

There is one more twist that gets people interested.

Sometimes your lender can use seller credits to buy down your interest rate instead of just wiping out fees.

For example:

- The seller gives you $10,000 dollars in credits

- Your lender uses that money, within program rules, to reduce your interest rate

- A lower rate can drop your monthly payment more than a small price reduction would in some situations

So, after we looked at the numbers together, you could potentially take $10,000 off the purchase price and save a little each month, or use $10,000 in credits to lower the rate and save more each month.

It's important to note that it doesn't always play out that way. The cost of a buydown and its impact on your rate change over time. Sometimes the better move is the price cut. Sometimes the better move is the buydown.

The important thing is this: you do not have to guess. Your lender can show you both choices on the same screen for your specific loan, so you can see which one feels better for your life.

When $10,000 Off The Price Usually Wins

You might lean toward a price reduction when:

- You plan to stay in the home for a long time

- You already have the cash needed to close and still keep a cushion

- You care most about paying less interest in the long run

- The appraisal feels a little tight and a lower price makes everyone more comfortable

In that situation, asking, "What does this look like with $10,000 off the price?" is a smart conversation to have.

When $10,000 In Closing Costs Usually Wins

You might lean toward seller-paid costs when:

- Coming up with the cash to close is your biggest stress

- Emptying your savings account would leave you awake at night

- You want a little breathing room after closing for furniture, paint, or a new snowblower

- Your lender can use part of that $10,000 to improve your interest rate in a way that meaningfully reduces your payment

In that situation, asking, "What happens if the seller helps with $10,000 toward my costs instead?" can open up options that feel more comfortable.

What Sellers And Appraisers See

Buyers are not the only ones looking at your numbers. Sellers and appraisers see two different stories, too.

From a seller's point of view:

- A lower price can feel like they are giving up ground

- A full price offer with credits lets them say, "We sold for this price," even though their net is lower

From an appraiser's point of view:

- They look at the contract price and recent sales

- They note any seller-paid costs in the contract

- They make sure those credits fit inside the guidelines for your loan program

The good news is, you do not have to manage that part. Your lender and I monitor those limits and help structure the offer so it complies with current rules.

If you are curious about broader homeownership programs or assistance that might apply to you, it can also be worth reviewing county and state homeownership assistance programs in North Dakota and Minnesota, along with City of Fargo home buyer resources and similar information from local cities.

Your job is to be clear about what matters most to you so your team can build the offer around that.

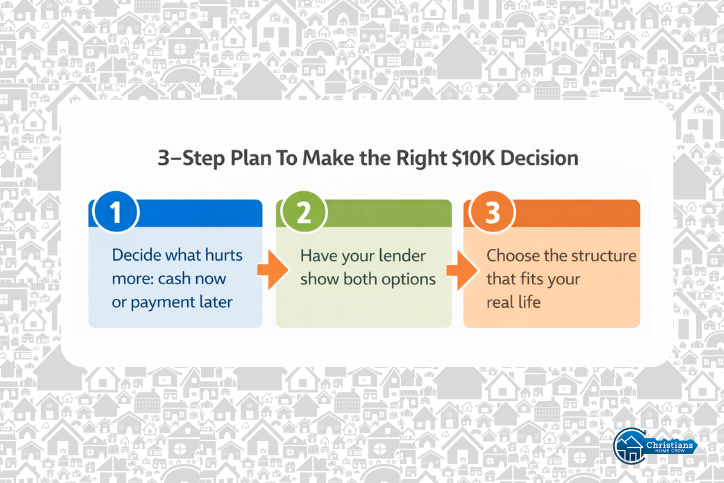

A Simple Plan To Make The Right 10K Decision

Here is a simple plan you can follow.

Step 1: Decide what hurts more right now

- Is your bigger worry cash to close?

- Or is it the monthly payment and total interest over time?

Be honest about which one keeps you up at night.

Step 2: Have your lender show you both options on one page

Ask them to run for a specific house you are considering:

- $10,000 off the price

- $10,000 in seller-paid costs, and if it makes sense, a rate buydown option

Looking at your own numbers side by side is where things usually click.

Step 3: Choose the structure that fits your life, not internet rules

There is no one rule that works for every buyer, every market, and every home.

If you are getting ready to write an offer in the Fargo, Moorhead, or West Fargo area and you are staring at this $10,000 decision, you do not have to walk through it alone.

Reach out, and we can sit down with your lender for a quick look at both paths.

When you understand the difference between $10K off the price and $10K toward your costs, you stop feeling like you might be making a $10,000 mistake and start feeling like you are making a thoughtful move for your future.

![]()

Let's connect!

Reach out today by email

or by calling (701) 373-5155

This article is for general informational purposes only and is based on common loan structures and examples that may or may not apply to your situation. It is not legal, tax, or financial advice, and it is not a commitment to lend or a guarantee of any particular interest rate, payment amount, or loan approval.

Loan guidelines, interest rates, costs, and eligibility rules change frequently and can vary between lenders and programs in North Dakota, Minnesota, and elsewhere. Always talk with your own licensed lender, and when appropriate your tax professional or attorney, about your specific situation before making decisions about how to structure an offer or loan.